The Income Tax Act, 1961 allows taxpayers to seek relief for delays in filing Income Tax Returns (ITRs) under certain conditions. Section 119(2)(b) enables individuals and entities to apply for condonation of delay by submitting an application to the appropriate income tax authority based on jurisdiction and monetary limits. Here’s a comprehensive guide to ensure a smooth filing process.

What is Section 119(2)(b)?

Section 119(2)(b) of the Income Tax Act, 1961 empowers income tax authorities to condone delays in filing ITRs if there is a genuine reason and hardship caused to the taxpayer.

Steps to Apply for Condonation

√Determine the Jurisdiction

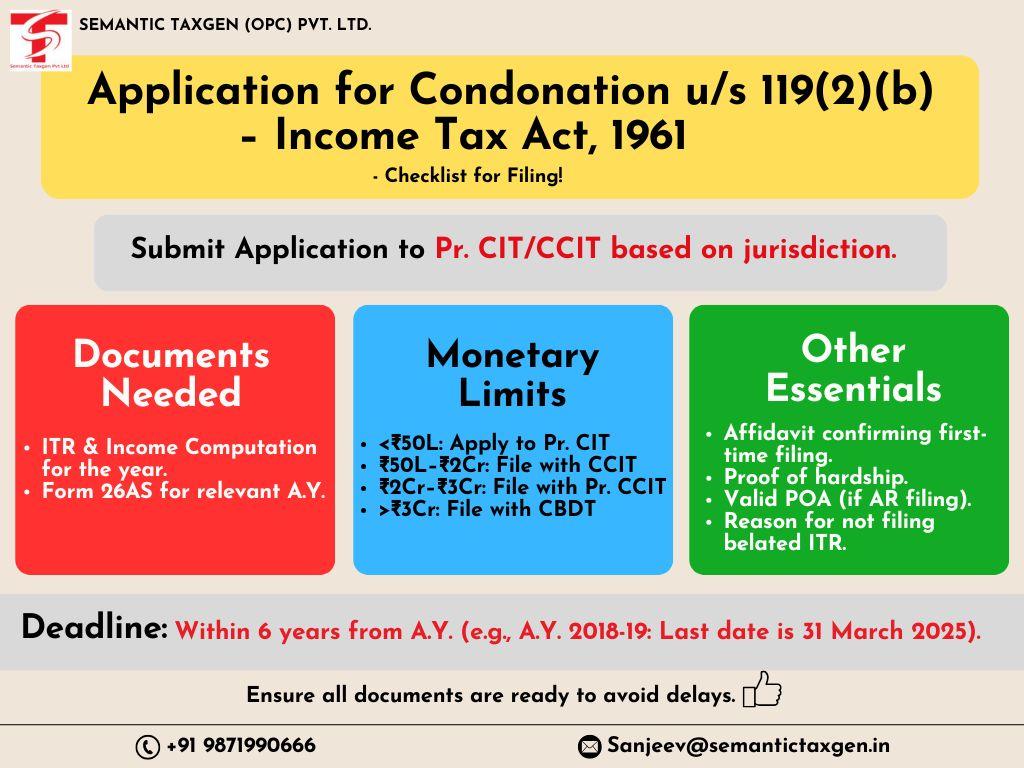

Submit your application to the appropriate authority based on the monetary limits:

- For income up to ₹50 lakhs: Apply to the Principal Commissioner of Income Tax (Pr. CIT).

- For income between ₹50 lakhs and ₹2 crores: Apply to the Chief Commissioner of Income Tax (CCIT).

- For income between ₹2 crores and ₹3 crores: Apply to the Principal Chief Commissioner of Income Tax (Pr. CCIT).

- For income above ₹3 crores: File the application with the Central Board of Direct Taxes (CBDT).

√Prepare Required Documents

Ensure you have the following documents:

- Copy of the Income Tax Return (ITR) and Income Computation for the relevant assessment year.

- Form 26AS for the applicable assessment year.

- An affidavit confirming that it is the first-time filing of the ITR.

- Proof of hardship caused due to non-filing.

- Power of Attorney (POA) if an Authorized Representative (AR) is filing the application on your behalf.

- A detailed reason for not filing the belated ITR.

√Draft the Application

Write a concise and clear application addressed to the appropriate authority, explaining the delay, its reasons, and attaching the required documents.

Key Considerations While Filing the Application

√Affidavit

A sworn statement confirming it is your first attempt to file the return ensures the credibility of your case.

√Reason for Delay

Clearly explain the circumstances leading to the delay. Examples include medical emergencies, loss of financial records, or unforeseen personal hardships.

√Proof of Hardship

Provide evidence showing how the delay caused genuine hardship, such as financial penalties or inability to claim a tax refund.

√Monetary Limits

Ensure you apply to the correct authority based on the quantum of income involved to avoid rejection due to jurisdictional errors.

√Timely Filing

Once the application is accepted, promptly file your ITR to avoid further complications.

Why is Condonation Important?

Condonation of delay allows taxpayers to:

- Claim missed refunds.

- Regularize tax compliance.

- Avoid unnecessary penalties or legal issues.

Conclusion

Filing an application under Section 119(2)(b) can help resolve issues stemming from delayed ITR submissions. By adhering to the outlined steps, ensuring proper documentation, and providing genuine reasons for the delay, taxpayers can increase the chances of approval.

For professional assistance, consult a tax advisor or authorized representative to streamline the process.

DISCLAIMER: The information provided in this article is intended for general informational purposes only and is based on the latest guidelines and regulations. While we strive to ensure the accuracy and completeness of the information, it may not reflect the most current legal or regulatory changes. Taxpayers are advised to consult with a qualified tax professional or you may contact to our tax advisor team through call +91-9871990777 or info@semantictaxgen.in