Phone++91 9654831210

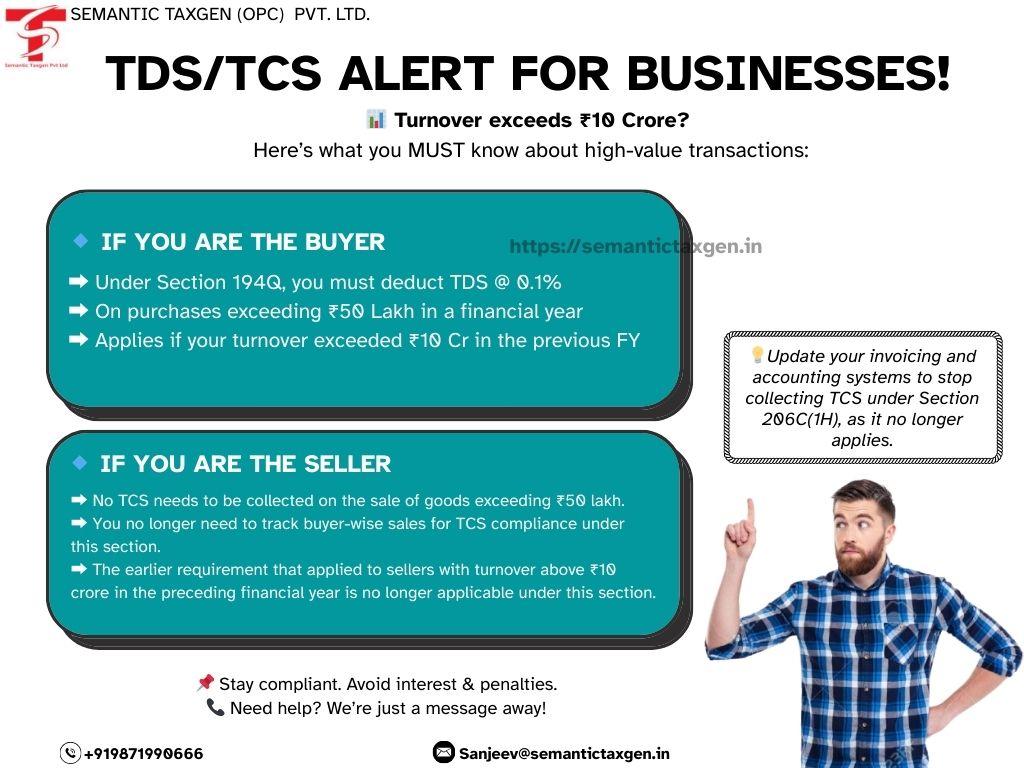

Are you a business with a turnover exceeding ₹10 crore? If so, there are crucial updates related to TDS and TCS compliance that you need to be aware of for high-value transactions. These updates can directly impact how you handle purchases and sales in your accounting and invoicing systems.

TDS Applicability for Buyers – Section 194Q

TDS Applicability for Buyers – Section 194QIf you are the buyer, the provisions of Section 194Q of the Income Tax Act apply to you:

Tip: Ensure your ERP or accounting software flags such transactions to comply with TDS deduction timelines.

Tip: Ensure your ERP or accounting software flags such transactions to comply with TDS deduction timelines.

No TCS Required for Sellers – Section 206C(1H)

No TCS Required for Sellers – Section 206C(1H)If you are the seller, here’s the major update:

This update significantly reduces the compliance burden for sellers who were previously required to maintain detailed buyer-wise sales reports and collect TCS accordingly.

This update significantly reduces the compliance burden for sellers who were previously required to maintain detailed buyer-wise sales reports and collect TCS accordingly.

What Should You Do?

What Should You Do?Update your invoicing and accounting systems immediately to reflect these changes:

Summary of Action Points

Summary of Action PointsRole | Applicable Section | Requirement |

Buyer | Section 194Q | Deduct TDS @ 0.1% if purchase > ₹50 lakh |

Seller | Section 206C(1H) | No need to collect TCS on goods sold |

Everyone | — | Update software and internal processes |

Stay Compliant. Stay Informed.

For expert guidance on TDS/TCS compliance, tax audits, or system updates, get in touch with Semantic Taxgen – your trusted partner in tax and accounting solutions.