About the GST credit set off while filing return, is there any possibility that we can change it at the time filing of Return.

Input Tax Credit, Ministry of Finance brought changes in the procedure of the order of set-off of the similar order and the said change came into force with effect from 29-03-2019. These new rules were set for minimizing the balance lying under IGST credits so that a balance could be achieved in distribution with the Centre and state. However, if this mechanism of off-setting is not understood and well managed, the businesses could end up with high working capital. It is therefore necessary that the order of utilization of input tax credit is understood, how best it could be optimally utilized and the resultant bearing on the business.

The amendments of the Law No. 208 concerning the Order of ITC Set-Off

The order of their utilization has been specifically explained through a CGST Circular No. 98/17/2019 issued on 23 April 2019. For instance, it further stated that before the commencement of the Rule 88A of the CGST Rules concerning the preservation of electronic liability on the GST portal, the taxpayers were required to follow the only facility available on the GST portal up to July 2019. The facility was enabled for computation in respect of returns filed after July 2019.

Firstly, as a way of introduction to both sections that have been incorporated in the CGST Act-,

√ “Section 49A: Despite anything contained in section 49, the input tax credit in respect of the central tax, the State tax or the Union territory tax shall be adjusted against the integrated tax, the central tax, the State tax or the Union territory tax as the case maybe, only after the input tax credit available on account of integrated tax has been fully utilized for such adjustment.

√Section 49B: Provided, however, that nothing contained in this Chapter shall take effect unless the order and manner of utilizing input tax credit under integrated tax, central tax, a State or a Union territory tax, as the case may be towards the payment of any such tax, is prescribed by the Government on the recommendations of the Council under clause (e) and clause (f) of sub-section (5) of section 49.

Later on, the above new provision has been added under rule 88A in the CT notification no. 16/2019 dated 29-03-2019.

√Rule 88A: Sequence of utilizing input tax credit: – The input tax credit on integrated tax has to be applied to the integrated tax payable and the balance if any, can be used to discharge central tax, and or State tax or Union territory tax as the case may be without any priority. Subject to the condition that the input tax credit on account of central tax, State tax or Union territory tax shall be admissible only when the input tax credit available on account of integrated tax has been fully adjusted against the payment of integrated tax and the amount of central tax, State tax or Union territory tax, as the case may be.

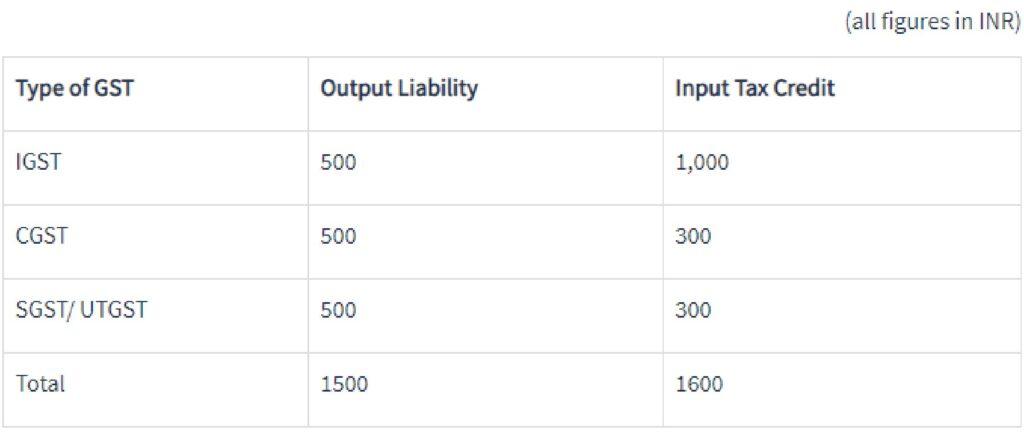

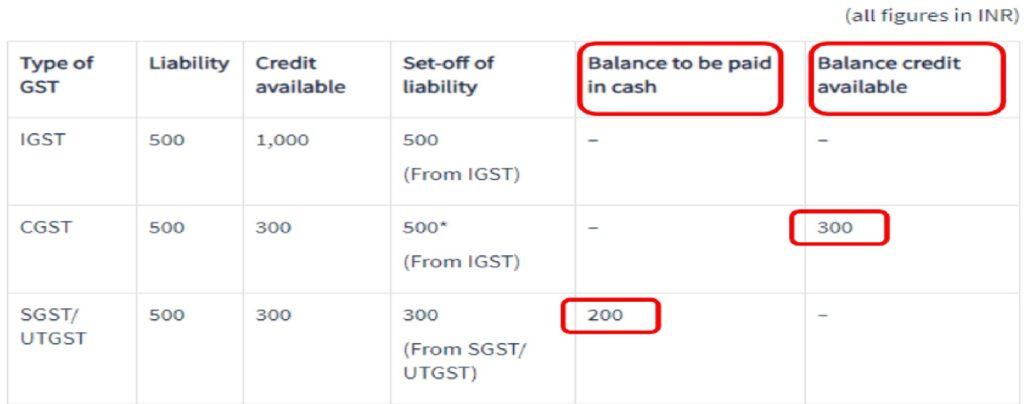

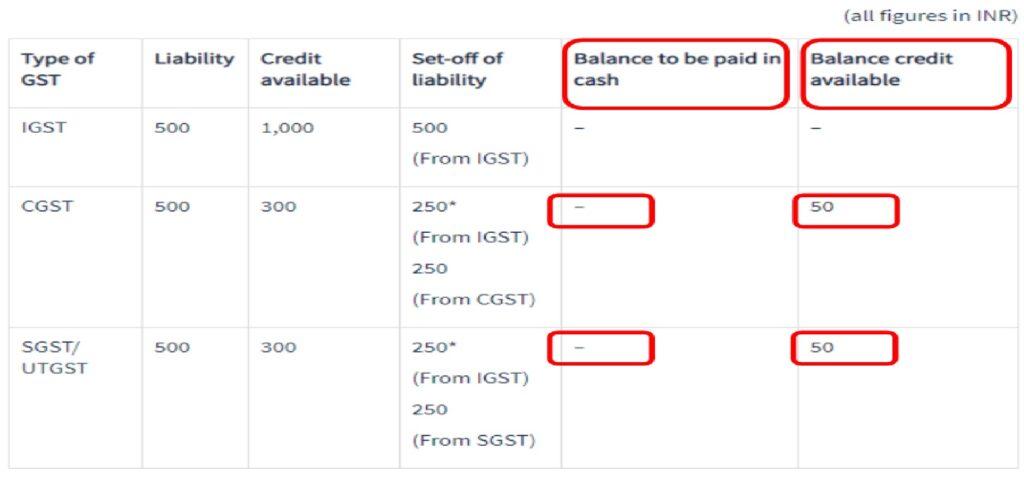

Input tax credit is another significant section where I’ll demonstrate how to set it off.

Let’s understand the impact of New Rule with the help of an illustration:

Assume that Mr. X liable for the following: and the input tax credit amount for the period is as follows: