Phone++91 9654831210

In this article we will discuss about the new invoice management system in GST, The current Goods and Services Tax (GST) structure in India will face alterations from October 1, 2024, which involves the overall efficiency of invoices used to help out in compliance. As Known in the recent amendments, new regulations introduce a much more digital and formalized approach towards invoice creation and submission process. It briefly examines the main characteristics of these trends and the effect they have on companies.

As from October 1, 2024, the GST framework will extend a mandatory use of the Invoice Management System (IMS). This new system will help to standardise the procedure in invoicing, uploading, and validation so that it becomes easier to deal with GST regulations. The IMS is the system to increase the transparency of the tax administration process, decrease the number of errors, and increase productivity.

From 1 st October 2024, the new IMS feature will be integrated into the GST portal where it is hoped that the system will work as follows:

As per the taxpayers and other relevant research scholars, one of the key issues that are existing in GST compliance is the availment of input tax credit (ITC). The IMS functionality is expected to address some of the critical bottle-necks in that process.

√Businesses will be required to submit invoices to the IMS portal, in real-time.

√Here, the system shall help in checking the invoices for compliance with the existing GST laws, minimizing on the mistakes that could be generated by the users.

Among these changes, the most important one is the demand in reporting invoices in real time. In the new regime, what archaic system had allowed generation of GST return, even without uploading of invoices to the GST portal, businesses will have to upload every invoice that they issue. Others are to reduce cases of invoice mismatches through real-time reporting to, for the purpose of tax administration, aims at achieving timely and accurate data.

Upcoming new IMS system is going to be synchronized with the e-way bill system so the information flow and in invoice generation and goods transportation will be in tandem. This integration will be useful in proper monitoring and control of movement of goods and thus reduce on instances of tax evasion. Companies will require that the systems of invoicing and logistic which they have will be compatible with this integration needed.

While governmental invoices have been already electronic since January 1 2014, the requirement of new functionality that is having an ability to digitally sign the invoices using a secure digital signature starts since October 1, 2024. This measure needs to be implemented to guarantee the genuineness and the sanctity of the invoices. By so doing the digital signature will act as a safeguard in ensuring that the invoices are not altered with or tampered in any way thereby protecting against fraud.

According to the new regulations there will be rigorous definition of compliance and increased punishments for violation of the requirements. Non-compliance with the real-time reporting and digital signature standards may attract severe penalties and fines to the business organizations. This makes it important for businesses to implement changes to their accounting systems and structures to separate with the national and international regulations that relate to them to avoid penalties.

√The IMS will be equipped with a highly interactive tool bar that will make it’s easy to use and easy to navigate.

√Training resources and support services will be provided in order to assist the users to easily move from the existing network.

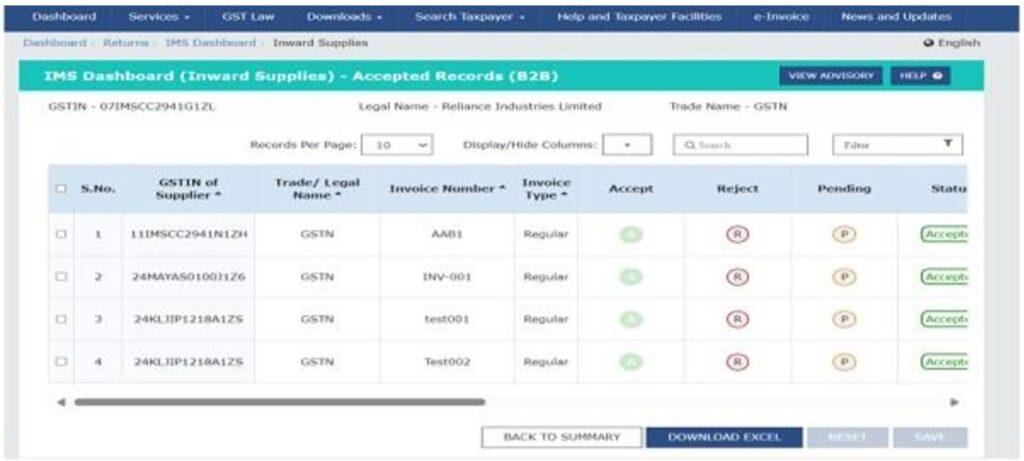

That’s How IMS Dashboard looks like:

Below is a screenshot of the IMS Dashboard, showcasing its key functionalities:

Note: The screenshot above is a representative image and may not reflect the final design of the IMS Dashboard.

All the recipient taxpayers including the QRMP taxpayers can access the functionality of IMS.

The implementation of the Invoice Management System (IMS) effective October 1, 2024, marks a significant shift in GST compliance and invoice management. By transitioning to real-time reporting, integrating with the e-way bill system, and mandating digital signatures, the new regulations aim to enhance transparency, reduce fraud, and streamline the tax administration process. Businesses should proactively adapt to these changes to ensure smooth compliance and avoid penalties.

DISCLAIMER: The information provided in this article is intended for general informational purposes only and is based on the latest guidelines and regulations. While we strive to ensure the accuracy and completeness of the information, it may not reflect the most current legal or regulatory changes. Taxpayers are advised to consult with a qualified tax professional or you may contact to our tax advisor team through call +91-9871990777 or info@semantictaxgen.in

© 2013-25 Semantic Taxgen Pvt Ltd - All Rights Reserved